🌍 Decoding Bitcoin’s Tax Status: Different Countries, Different Rules

Imagine embarking on a journey around the globe, with each country you visit having its own set of rules on how to treat your Bitcoin. Just like the various cuisines, languages, and cultures you’d encounter, every country approaches Bitcoin taxation in its unique way. From the sunny shores of Australia, where Bitcoin is seen as property and subject to capital gains tax, to the bustling streets of Germany, where it’s treated more like currency, providing tax exemptions if held for more than a year. Navigating this landscape isn’t just about knowing where you stand but understanding the global patchwork of regulations that affect your digital wallet. It’s like piecing together a puzzle where each piece is shaped by the legal and financial mindset of a country. Keeping up with this mix of rules isn’t just good practice; it’s essential for anyone looking to tread the international Bitcoin waters without running aground on tax issues.

| Country | Taxation Approach |

|---|---|

| Australia | Property – Subject to Capital Gains Tax |

| Germany | Currency – Tax Exempt if held > 1 year |

| USA | Property – Subject to Income and Capital Gains Tax |

🤔 Why Keeping Tabs on Your Bitcoin Matters

Imagine finding a treasure chest but not knowing it’s worth. That’s a bit like having Bitcoin and not keeping tabs on it, especially when tax time rolls around. Different countries view Bitcoin in various lights, some as property, others like currency, and this affects how it’s taxed. If you don’t keep an eye on your Bitcoin’s journey—how much you got it for, how much it was worth when you used it or sold it—you might end up in a tangled web, unsure how much tax you owe or even facing penalties for not reporting it correctly. It’s not just about following rules; it’s about being smart. Knowing your situation helps you plan better, like when’s the best time to sell or use your Bitcoin to make the most of your investment. Plus, with https://wikicrypto.news/decentralization-debate-bitcoins-advantage-over-fiat-currency, you can find ways to manage your Bitcoin with an eye towards privacy, keeping you a step ahead.

💡 Simplified Breakdown: Calculating Your Bitcoin Taxes

So, you’ve got some Bitcoin, and now it’s time to figure out how much of it you need to share with the tax folks, right? Think of it as a recipe where the ingredients are your Bitcoin activities. First, mix in how much you initially paid for your Bitcoin, this is like your base. Then, stir in the current value when you decide to use or sell it. The difference between these two is your gain, kind of like how much your dough has risen. Now, here’s where it can get a bit spicy. The tax rate you sprinkle on top will depend on how long you’ve held onto your Bitcoin. If it’s been a short time, you might pay more, like adding a bit of extra seasoning for a stronger flavor. But keep an eye out! 🌱👀 Just like in cooking, you don’t want to miss any steps or forget any ingredients, such as reporting gifts or payments in Bitcoin, because that could lead to a recipe disaster. And remember, this is a basic dish; some of you might have more complex recipes based on where you live or how you use your Bitcoin.🌎🔍

🌱 from Miners to Traders: Who Owes What?

In the world of Bitcoin, everyone from the bedroom miners to big-time traders plays a part in the intricate dance of digital currency. Imagine miners as the gold diggers of the digital age, where instead of shovels and pickaxes, they use powerful computers to solve complex puzzles, earning Bitcoin as their treasure. Now, once these digital coins are mined, they enter the vast sea of the market, where traders—big and small—try to navigate the waves, buying low and selling high. But here’s the twist: whether you’re unearthing digital gold or playing the markets, the taxman is interested in your treasure. Each country waves its own flag of rules when it comes to taxation, making it essential for everyone in the Bitcoin game to stay informed and compliant.

This brings us to an essential aspect often overlooked: bitcoin privacy concerns. Maintaining anonymity and protecting your digital assets becomes paramount, especially when dealing with taxation. For those looking to dive deeper into keeping your Bitcoin secure and private, consider exploring the differences between cold storage and hot wallets. A great starting point is this detailed guide: bitcoin privacy concerns suggestions. Understanding these concepts not only helps in safeguarding your assets but also in navigating the complex web of tax obligations. From understanding your tax liabilities as a miner to recognizing the nuances of trading tax implications, arming yourself with knowledge is key. Remember, in the ever-evolving landscape of Bitcoin taxation, staying informed is your best strategy.

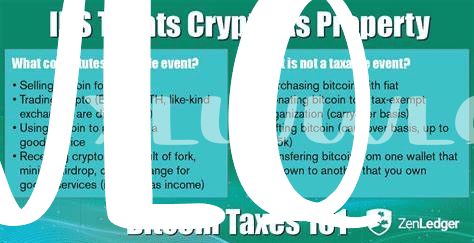

🛑 Common Pitfalls to Avoid in Bitcoin Taxation

Navigating the maze of bitcoin taxation can sometimes feel like trying to solve a complex puzzle with missing pieces. One major slip-up many folks encounter is not keeping detailed records of their transactions. Think of it as trying to piece together a giant jigsaw without the picture on the box; without a clear record of when you bought, sold, or used your bitcoin, calculating how much tax you owe becomes guesswork. This isn’t just about knowing your profits or losses but also about being able to prove those numbers to the tax authorities if they ask.

Another area where many stumble is not understanding that different types of bitcoin activities can be taxed differently. For example, mining bitcoin and trading it on an exchange are not viewed the same in the eyes of tax laws. Here is a simple breakdown:

| Activity | Tax Consideration |

|———-|——————-|

| Mining | May be taxed as income |

| Trading | May be subject to capital gains tax |

| Spending | Could be seen as selling, possibly triggering capital gains |

Failing to appreciate these distinctions can lead to unpleasant surprises come tax season. To make matters more complex, splurging your digital cash on purchasing goods or services might trigger a capital gains event, much like selling your bitcoin would. It’s like discovering a hidden trap in a game just when you thought you were scoring points. Always remember, staying informed and organized is your best strategy in winning the bitcoin tax game.

🚀 Future Trends: How Bitcoin Taxation Might Change

As we look toward the horizon, the landscape of Bitcoin taxation is poised for an evolution. With governments around the world beginning to realize the significance of cryptocurrencies, we might soon see a shift in how these digital assets are taxed. Currently, the approach to Bitcoin taxation is as varied as the countries themselves, creating a patchwork quilt that can be challenging to navigate. However, there’s a growing conversation among international tax authorities aimed at harmonizing these rules to simplify compliance for individuals and businesses alike. This could mean anything from standardized tax rates for Bitcoin earnings to streamlined reporting processes that make it easier for people to declare their digital currency activities.

For those keeping an eye on the future, understanding the nuances of how Bitcoin operates in comparison to traditional money will be crucial. This knowledge will not only help in making informed decisions but also in navigating the tax implications more smoothly. For a deeper dive into the differences between digital and fiat currencies, checking out bitcoin wallet types suggestions can provide valuable insights. Moreover, as the digital currency sphere continues to mature, staying updated on these changes will be key for anyone involved in mining, trading, or using Bitcoin, helping to avoid common pitfalls and ensure compliance with the ever-evolving tax regulations.